Executive Orders & Federal Regulations

How presidential directives translate into regulatory outcomes — and who shapes policy through the rulemaking process.

Show me Trump's AI export Executive Order — who does it affect and what do they need to do?

Trump's AI Export Executive Order: Who It Affects & What They Need to Do

The EO Landscape

PoliStack's graph contains 8 Trump-era AI executive orders spanning both terms. The core export-focused EO is EO 14320 — "Promoting the Export of the American AI Technology Stack" (signed July 23, 2025), flanked by two companion orders signed the same day: EO 14319 ("Preventing Woke AI in the Federal Government") and a data center permitting order. A December 2025 order (EO 14365) added state preemption. Together, these form a unified AI industrial policy.

The PoliStack graph maps EO 14320 to 13 issue areas — from Science/Technology and Trade to Defense, Intelligence, Manufacturing, Financial Institutions, and Small Business — signaling just how many sectors are in scope.

Who's Affected (from the EO full text + 181 public comments in PoliStack)

1. U.S. AI Companies Forming Export Consortia

This is the primary affected group. EO 14320 Section 3 directs Commerce to issue a public call for proposals from industry-led consortia to deliver "full-stack" AI export packages. Each proposal must include:

- AI-optimized hardware (chips, servers, accelerators) — with disclosure of U.S. manufacturing content

- Data pipelines and labeling systems

- AI models and systems

- Cybersecurity measures for AI models

- Sector-specific applications (healthcare, education, agriculture, transportation)

- Target countries or regional blocs

- A business/operational model for data center ownership and operation

- Requested federal incentives

- Full compliance with U.S. export control regimes (50 USC Ch. 58, BIS guidance)

The regulations.gov docket (ITA-2025-0070) generated by this EO received 181 public comments — all classified as "high significance" in PoliStack's regulatory graph. The commenters reveal who's actually positioning for this:

| Commenter Type | Examples | What They Want |

|---|---|---|

| Chipmakers | Intel | Prioritize U.S.-based manufacturing; finance domestic fabs |

| AI hardware | Groq, Tenstorrent | Pre-cleared "Trusted Stack Provider" status; expedited export licenses; include SMEs |

| Cloud/infra | Kyndryl, SHI International, Vertiv | Expand stack to include physical infrastructure (power, cooling, modular data centers) |

| AI software | Cognition AI, Snorkel AI, inmind.ai | Clear export-license pathways for agentic AI; elevate data layer as core pillar |

| Governance/trust | Credo AI, DocuSign, Lucid Computing | Add "Trust Layer" and "Verification & Attestation Layer" to the stack definition |

| Semiconductor trade | SEMI (3,300+ members) | Include mature-node semiconductors, energy/thermal tech; define "American" |

| Telecom | CTIA | Recognize connectivity/network layer as essential; allocate mid-band spectrum |

| Trade associations | TechNet (100+ companies), U.S. Chamber | Define "consortium" and "U.S. AI stack"; protect non-consortium firms from disadvantage |

| Think tanks | CNAS, Institute for Progress | Target "swing markets" (Brazil, Egypt, Indonesia); cloud-first deployments |

| Music/IP | RIAA | Protect copyright; oppose TDM exceptions for AI training |

| Foreign-market consultants | PS-engage, SoKat, A&M NST | ASEAN/Africa-specific deployment guidance; governance frameworks |

| Small businesses | IDARE LLC, iQuasar, Economic Dev. Collaborative | Financing, export insurance, regulatory navigation for SMEs |

| Commenter Type | Examples | What They Want |

|---|---|---|

| Chipmakers | Intel | Prioritize U.S.-based manufacturing; finance domestic fabs |

| AI hardware | Groq, Tenstorrent | Pre-cleared "Trusted Stack Provider" status; expedited export licenses; include SMEs |

| Cloud/infra | Kyndryl, SHI International, Vertiv | Expand stack to include physical infrastructure (power, cooling, modular data centers) |

| AI software | Cognition AI, Snorkel AI, inmind.ai | Clear export-license pathways for agentic AI; elevate data layer as core pillar |

| Governance/trust | Credo AI, DocuSign, Lucid Computing | Add "Trust Layer" and "Verification & Attestation Layer" to the stack definition |

| Semiconductor trade | SEMI (3,300+ members) | Include mature-node semiconductors, energy/thermal tech; define "American" |

| Telecom | CTIA | Recognize connectivity/network layer as essential; allocate mid-band spectrum |

| Trade associations | TechNet (100+ companies), U.S. Chamber | Define "consortium" and "U.S. AI stack"; protect non-consortium firms from disadvantage |

| Think tanks | CNAS, Institute for Progress | Target "swing markets" (Brazil, Egypt, Indonesia); cloud-first deployments |

| Music/IP | RIAA | Protect copyright; oppose TDM exceptions for AI training |

| Foreign-market consultants | PS-engage, SoKat, A&M NST | ASEAN/Africa-specific deployment guidance; governance frameworks |

| Small businesses | IDARE LLC, iQuasar, Economic Dev. Collaborative | Financing, export insurance, regulatory navigation for SMEs |

2. Federal Agencies (EO 14319 — "Preventing Woke AI")

Every federal agency that procures LLMs is directly affected. Section 3 mandates they procure only LLMs meeting two principles:

- Truth-seeking: Historical accuracy, scientific objectivity, acknowledgment of uncertainty

- Ideological neutrality: No encoded partisan judgments unless prompted by the user

OMB must issue implementing guidance within 120 days. After that, agencies must include these terms in every new LLM contract and revise existing ones. Vendors that fail to comply face decommissioning costs charged back to them.

3. AI Vendors Selling to the U.S. Government

LLM developers (Anthropic, OpenAI, Google, Meta, etc.) must demonstrate compliance with the "Unbiased AI Principles" to keep or win federal contracts. The EO explicitly allows vendors to comply through disclosure of system prompts, specifications, or evaluations — but avoids requiring model weight disclosure.

4. State Governments (EO 14365 — December 2025)

The December EO creates three enforcement mechanisms against state AI laws:

- AI Litigation Task Force at DOJ (within 30 days) to sue states whose AI laws conflict with federal policy — specifically targeting laws that "require AI models to alter their truthful outputs" (e.g., Colorado's algorithmic discrimination law)

- Funding restrictions: States with "onerous AI laws" become ineligible for BEAD broadband funding

- Federal preemption: FCC directed to consider a federal AI reporting/disclosure standard that preempts state laws; FTC directed to issue policy on when state laws forcing "deceptive" AI outputs are preempted

The only carve-outs: child safety, data center infrastructure, and state government's own AI procurement.

5. Chipmakers and Semiconductor Exporters

While EO 14320 is the export promotion order, the broader Trump AI policy rescinded the Biden-era "AI Diffusion Rule" (three-tier country controls) in May 2025 and replaced it with country-by-country negotiations plus a revenue-sharing mechanism (25% of H200 sales to China). PoliStack's bill search surfaces active 119th Congress legislation responding to this:

- S 3374 (SAFE Chips Act) — Sen. Ricketts (R-NE), 9 cosponsors, Banking Committee

- HR 5022 (No Advanced Chips for the CCP Act) — Rep. Krishnamoorthi (D-IL)

- S.Res. 598 — Sen. Warren (D-MA), condemning the UAE AI chip export deal citing national security and conflict-of-interest

6. The Economic Diplomacy Action Group (EDAG)

EO 14320 Section 4 directs the EDAG to deploy federal financing tools — EXIM loans, DFC equity investments and political risk insurance, and technical assistance — in support of selected AI export packages. This means the SBA, State Department, EXIM Bank, and DFC all become active players in AI export facilitation.

What They Need to Do — The Compliance Timeline

| Deadline | Who | Action Required |

|---|---|---|

| Oct 21, 2025 | Commerce | Establish the American AI Exports Program |

| Oct 28, 2025 | Commerce (done) | Issue RFI for public comment (ITA-2025-0070) — 181 comments received |

| 90 days after RFI | Industry consortia | Submit proposals responding to Commerce's call |

| 120 days of EO 14319 | OMB | Issue guidance implementing "Unbiased AI Principles" for federal procurement |

| 90 days after OMB guidance | Federal agencies | Adopt procedures ensuring procured LLMs comply |

| 30 days of EO 14365 | DOJ | Establish AI Litigation Task Force |

| 90 days of EO 14365 | Commerce | Publish evaluation of "onerous" state AI laws |

| 90 days of EO 14365 | Commerce/NTIA | Issue BEAD funding eligibility notice excluding states with onerous AI laws |

| 90 days after state-law evaluation | FCC | Initiate proceeding on federal AI reporting standard that preempts state laws |

| 90 days of EO 14365 | FTC | Issue policy statement on when state AI laws are preempted by FTC Act |

| Ongoing | Chipmakers | Navigate per-country export controls, revenue-sharing conditions, end-use screening |

| Deadline | Who | Action Required |

|---|---|---|

| Oct 21, 2025 | Commerce | Establish the American AI Exports Program |

| Oct 28, 2025 | Commerce (done) | Issue RFI for public comment (ITA-2025-0070) — 181 comments received |

| 90 days after RFI | Industry consortia | Submit proposals responding to Commerce's call |

| 120 days of EO 14319 | OMB | Issue guidance implementing "Unbiased AI Principles" for federal procurement |

| 90 days after OMB guidance | Federal agencies | Adopt procedures ensuring procured LLMs comply |

| 30 days of EO 14365 | DOJ | Establish AI Litigation Task Force |

| 90 days of EO 14365 | Commerce | Publish evaluation of "onerous" state AI laws |

| 90 days of EO 14365 | Commerce/NTIA | Issue BEAD funding eligibility notice excluding states with onerous AI laws |

| 90 days after state-law evaluation | FCC | Initiate proceeding on federal AI reporting standard that preempts state laws |

| 90 days of EO 14365 | FTC | Issue policy statement on when state AI laws are preempted by FTC Act |

| Ongoing | Chipmakers | Navigate per-country export controls, revenue-sharing conditions, end-use screening |

The Strategic Picture

What makes this EO architecture distinctive is that it's simultaneously promoting exports and preempting domestic regulation — using federal financing to incentivize full-stack AI deployment abroad while using federal funding leverage (BEAD) and litigation (DOJ Task Force) to discipline states at home. The 181 public commenters on the American AI Exports Program RFI reveal an industry scrambling to shape the definition of what "full-stack" even means — with everyone from chipmakers to governance startups to music labels trying to get their component recognized as essential.

The PoliStack data makes clear this isn't a single executive order — it's a coordinated policy stack of 6+ Trump-era AI EOs, 2 active regulations at pre-rulemaking stage, and at least 8 responsive bills in the 119th Congress, none of which have advanced past committee.

Show me other EOs where there is huge participation by organizations and lobbyists. The EOs which have regulations are labeled and indexed.

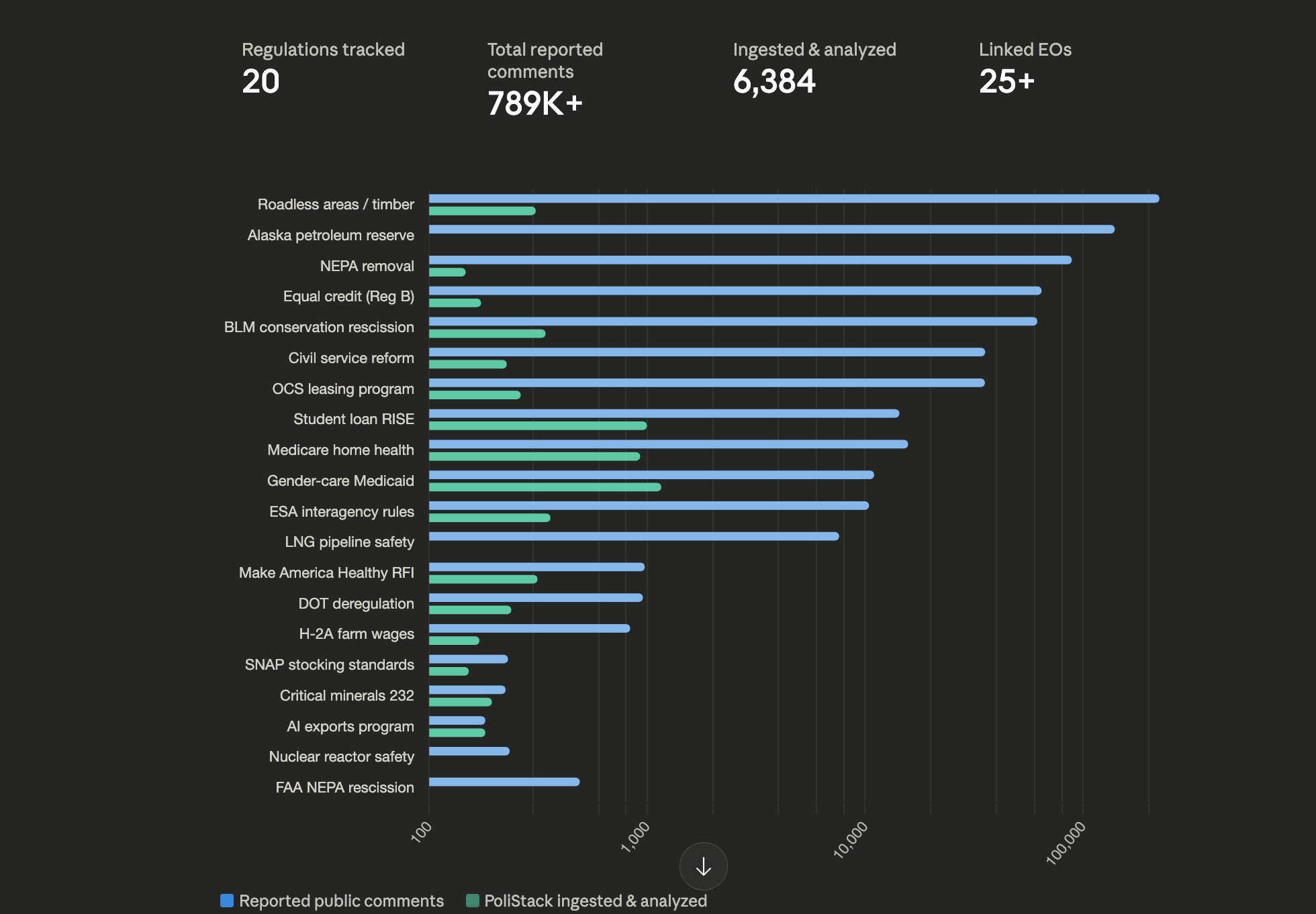

The Heavyweight EOs Driving the Most Regulatory Participation

Every regulation in this analysis was generated by an executive order — that EO → Regulation → Docket → PublicComment chain is what the PoliStack graph indexes.

Tier 1: Massive public response (50K+ comments)

The National Forest Roadless Areas regulation (linked to 4 EOs including "Immediate Expansion of American Timber Production" and "Unleashing American Energy") drew 223,862 comments — the single most commented regulation in the graph. The Alaska Petroleum Reserve rescission (139K), NEPA removal (88K), Equal Credit / Reg B rewrite under the anti-DEI EOs (64K), and BLM Conservation rescission (61K) round out the top tier.

Tier 2: High-stakes policy fights (10K–35K)

The Civil Service reform rule (Schedule F / Schedule G, linked to 6 EOs), the OCS leasing program for offshore drilling, and the Student Loan RISE rule each drew tens of thousands. The gender-care Medicaid ban (11K reported, 1,160 ingested and fully analyzed in PoliStack) is linked to three separate EOs — showing how the administration stacks multiple orders behind a single regulatory action.

Tier 3: Industry-specific, deeply analyzed (100–1K)

This is where PoliStack's ingested data is richest relative to the volume. The AI Exports Program (181 comments, all 181 ingested), Critical Minerals 232 investigation (224 reported, 194 ingested), and H-2A farmworker wages (836 reported, 170 ingested) have nearly complete analytical coverage — meaning every commenter's stance, sophistication, key positions, regulatory asks, and self-interest indicators are queryable in the graph.

Key Structural Insight

EO 14192 ("Unleashing Prosperity Through Deregulation") is the connective tissue — it's linked to 14 of these 20 regulations as a co-generating EO. It acts as a blanket deregulatory mandate that gives legal authority to virtually every rollback. If you want to track lobbying influence on Trump-era deregulation, that single EO is the hub node.

Show me who commented on the critical minerals Section 232 investigation (BIS-2025-0025). What are mining and defense firms asking for?

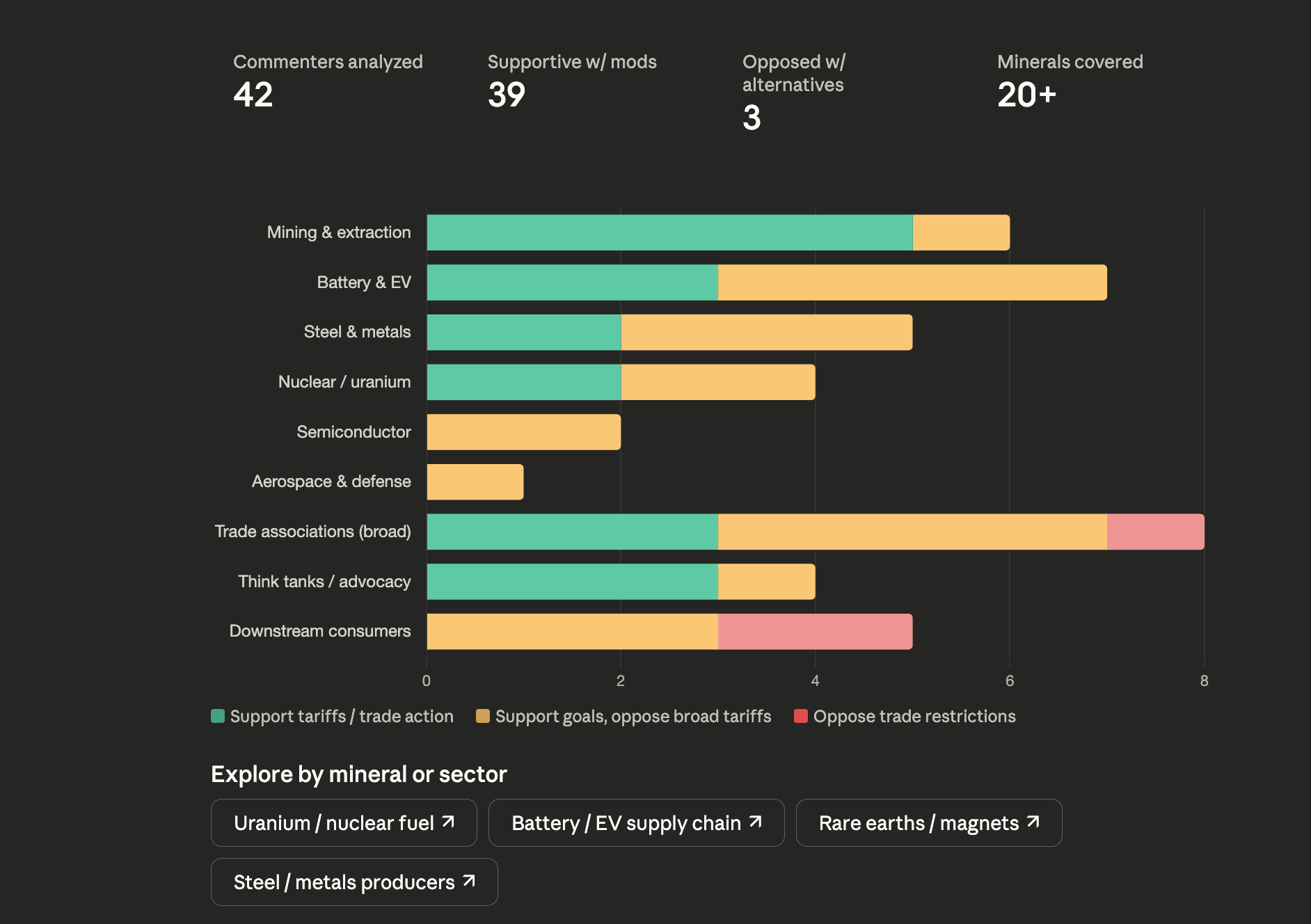

Critical Minerals Section 232 Investigation (BIS-2025-0025)

This docket is tied to EO 14272 — Trump's Section 232 investigation into processed critical minerals and derivative products, signed April 15, 2025. Of 194 ingested comments, the overwhelming pattern is "support the investigation, but don't hurt us with blunt tariffs."

The Fault Line: Upstream Producers vs. Downstream Consumers

The fundamental tension running through these comments is that miners and processors want tariffs to protect infant domestic capacity from Chinese dumping, while manufacturers who consume those minerals want exemptions to avoid crippling cost increases on inputs they can't source domestically yet.

Who Wants Tariffs

- MP Materials — operates the only scaled U.S. rare earth mine (Mountain Pass). Wants policy support to fill gaps in metalmaking, alloying, and magnet production. Planning HREE separation with DoD support.

- North American Graphite Alliance — China controls 92% of high-purity anode material. Wants tariffs and reversal of prior Section 301 exemptions for graphite that let Chinese supply dominate.

- Sila Nanotechnologies — U.S. silicon anode manufacturer. Wants tariffs specifically on silicon anode materials before Chinese state-subsidized competitors destroy their technological lead.

- Copper Development Association — wants tariffs on all semi-fabricated copper products (HTS Chapter 74) but exemptions on raw cathodes and scrap feedstock.

- Energy Fuels — operates the only U.S. facility processing monazite into REE oxides. Wants Section 232 authority used to support domestic processing and address circumvention of the Russian Uranium Ban.

- Bunker Hill Mining / Alliance for Mineral Security — the most aggressive asks: National Defense Price Indices, export controls on magnet scrap and battery black mass, ROFR-style stockpiling contracts, U.S.-backed SPVs for overseas mining investments.

Who Says "Not Yet" on Tariffs

- ZETA (50 EV supply chain companies) — members have $55 billion invested. Wants phased tariffs only after domestic alternative suppliers are qualified. Warns premature tariffs would harm battery supply chains for both automotive and military.

- SEIA — wants 3-year delay before tariffs on battery cells, modules, and graphite/lithium imports. Requests new HTS breakouts for lithium-ion batteries.

- Consumer Technology Association — 1,200+ tech companies. Calls Section 232 "the wrong tool" and wants consumer/commercial products excluded entirely.

- NAM (National Association of Manufacturers) — explicitly opposes immediate broad-based tariffs. Wants permitting reform, EXIM loans, and allied coordination instead.

- Aerospace Industries Association — warns that tariffs on aerospace-grade critical minerals where no domestic supply exists would harm defense readiness and export competitiveness.

Who Opposes Outright

- IPA (Platinum Group Metals Association) — wants PGMs fully excluded. Argues China has minimal involvement in PGM supply chains and tariffs would severely distort a small, specialized market.

- Umicore — recommends the President take no action to restrict imports. If forced, wants exemptions for automotive/defense, FTA-covered goods, and a full exclusion process.

- Korea Battery Industry Association — 238 Korean companies with $58.7B invested in the U.S. Wants a minimum 5-year exemption for Korean imports.

What Defense Firms Specifically Want

Defense-adjacent commenters share a common thread: secure supply without disrupting current procurement.

- Specialty Steel Industry of North America — strict enforcement of the Specialty Metals Amendment (10 U.S.C. §4863) requiring defense metals to be melted/produced in the U.S. Wants reciprocal defense procurement exemptions (MOUs letting allies bypass domestic sourcing) revisited and limited.

- Perryman Company (titanium mill products, 700 U.S. employees) — the U.S. has zero domestic titanium sponge production. Wants targeted trade measures on titanium and action against rising Chinese titanium imports.

- IperionX — wants tariffs on titanium products reversed from the 2019 finding that tariffs wouldn't help. Claims new technologies make domestic titanium from scrap viable now.

- Amaero (titanium/refractory metal powders) — wants DoD and DOE required to source domestically melted titanium and refractory alloys. Wants DPA Title III funding and tax credits grandfathered to January 2025 investments.

- MM Metals USA (low-carbon ferrochrome) — wants anti-dumping investigations on imported ferrochrome, export restrictions on aluminum scrap, and the material added to the National Defense Stockpile.

The Mineral-by-Mineral Picture

| Mineral | Key Commenters | Core Ask |

|---|---|---|

| Rare earths | MP Materials, Alliance for Mineral Security, Bunker Hill | Distinguish HREEs from LREEs; fund domestic refining/alloying; stockpile |

| Graphite | NAGA, Snorkel AI (from AI docket) | Tariffs on Chinese anode material; revoke Section 301 exemptions |

| Titanium | Perryman, IperionX, Amaero | Zero U.S. sponge production; tariffs + DPA funding for new tech |

| Uranium | Cameco, Centrus, Urenco, Energy Fuels, UPA | Block Russian/Chinese circumvention; fund domestic enrichment; exempt Canadian imports |

| Nickel | Outokumpu, Trafigura, Nyrstar | Outokumpu wants action against Indonesia/China; Trafigura opposes refined nickel tariffs |

| Copper | Copper Dev. Association | Tariffs on semi-fab products; exempt raw cathodes; export ban on high-purity scrap |

| PGMs | Johnson Matthey, Heraeus, IPA | Full exclusion from Section 232; account for recycling flows |

| Lithium/batteries | ZETA, BMTC, SEIA, Fluence, ACP | Phase tariffs; exempt stationary storage cells; target upstream minerals not finished products |

| Zinc | Nyrstar, South32 Hermosa | Import tariffs + price floors for refined zinc; incentivize domestic smelting |

| Mineral | Key Commenters | Core Ask |

|---|---|---|

| Rare earths | MP Materials, Alliance for Mineral Security, Bunker Hill | Distinguish HREEs from LREEs; fund domestic refining/alloying; stockpile |

| Graphite | NAGA, Snorkel AI (from AI docket) | Tariffs on Chinese anode material; revoke Section 301 exemptions |

| Titanium | Perryman, IperionX, Amaero | Zero U.S. sponge production; tariffs + DPA funding for new tech |

| Uranium | Cameco, Centrus, Urenco, Energy Fuels, UPA | Block Russian/Chinese circumvention; fund domestic enrichment; exempt Canadian imports |

| Nickel | Outokumpu, Trafigura, Nyrstar | Outokumpu wants action against Indonesia/China; Trafigura opposes refined nickel tariffs |

| Copper | Copper Dev. Association | Tariffs on semi-fab products; exempt raw cathodes; export ban on high-purity scrap |

| PGMs | Johnson Matthey, Heraeus, IPA | Full exclusion from Section 232; account for recycling flows |

| Lithium/batteries | ZETA, BMTC, SEIA, Fluence, ACP | Phase tariffs; exempt stationary storage cells; target upstream minerals not finished products |

| Zinc | Nyrstar, South32 Hermosa | Import tariffs + price floors for refined zinc; incentivize domestic smelting |

The Strategic Insight

Almost nobody opposes the investigation — the real battle is over remedy design. The upstream producers (miners, processors, smelters) want tariffs to create the economic conditions for domestic capacity. The downstream consumers (automakers, steelmakers, battery manufacturers, tech companies) want time, exemptions, and alternative policy tools (DPA funding, permitting reform, allied trade agreements) instead. The defense sector sits awkwardly in between — they need secure supply but can't afford supply disruptions to current weapons programs.

The most sophisticated commenters (Rio Tinto, CNAS-adjacent think tanks, SEMI) push a "friendshoring + targeted incentives" framework rather than blanket protectionism — pair preferential U.S. market access with binding supply commitments from allies, and use DPA/EXIM/DFC financing to underwrite domestic processing capacity.

Show me the organizations or lobbyists connected with docket BIS-2025-0025, linked to EO 14272

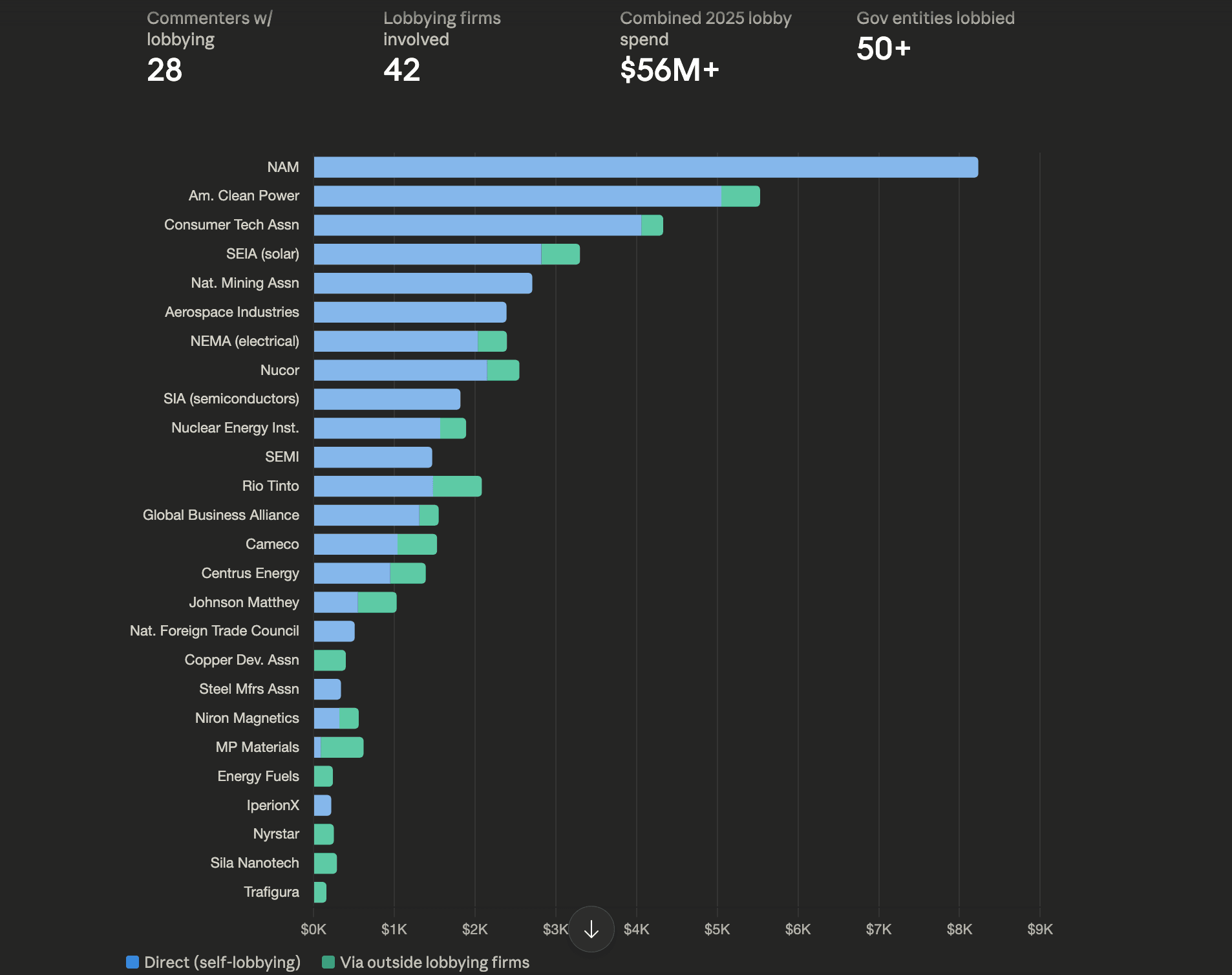

Lobbying Network: Docket BIS-2025-0025 × EO 14272

Every organization shown below both filed a public comment on docket BIS-2025-0025 and has registered lobbying activity in 2025 touching the same agencies that administer EO 14272.

The Dual-Track Influence Pattern

What the graph reveals is a coordinated comment + lobby strategy. These organizations don't just file a public comment and hope for the best — they're simultaneously running lobbying operations targeting the exact agencies that will decide the outcome.

The Heaviest Spenders Who Also Commented

| Commenter | 2025 Lobby Spend | Lobbying Firms | Key Gov Targets |

|---|---|---|---|

| NAM | $8.2M | Self-lobbying | Commerce, USTR, DOD, EPA |

| American Clean Power | $5.5M | Self + Lot Sixteen, Cassidy, Capitol Tax | Commerce, USTR, Energy, Senate |

| Consumer Tech Assn | $4.3M | Self + K&L Gates | Commerce, USTR, White House |

| SEIA | $3.3M | Self + Squire Patton Boggs | Commerce, Energy, USTR |

| National Mining Assn | $2.7M | Self-lobbying | Interior, BLM, Commerce, Energy |

| Nucor | $2.6M | Self + Wiley Rein + Strategic Marketing | Commerce, USTR, DOD, EPA, Energy |

| Aerospace Industries | $2.4M | Self-lobbying | DOD, Commerce, USTR, State |

| Rio Tinto | $2.1M | Self + Lot Sixteen + CGCN + Avoq + Torres + Holland & Hart | Commerce, USTR, Interior, Treasury, Energy, State, NSC, EXIM Bank |

| Nuclear Energy Inst. | $1.9M | Self + Miller Strategies | Energy, DOD, State, Commerce |

| SEMI | $1.5M | Self-lobbying | Commerce, USTR, DOD |

| Commenter | 2025 Lobby Spend | Lobbying Firms | Key Gov Targets |

|---|---|---|---|

| NAM | $8.2M | Self-lobbying | Commerce, USTR, DOD, EPA |

| American Clean Power | $5.5M | Self + Lot Sixteen, Cassidy, Capitol Tax | Commerce, USTR, Energy, Senate |

| Consumer Tech Assn | $4.3M | Self + K&L Gates | Commerce, USTR, White House |

| SEIA | $3.3M | Self + Squire Patton Boggs | Commerce, Energy, USTR |

| National Mining Assn | $2.7M | Self-lobbying | Interior, BLM, Commerce, Energy |

| Nucor | $2.6M | Self + Wiley Rein + Strategic Marketing | Commerce, USTR, DOD, EPA, Energy |

| Aerospace Industries | $2.4M | Self-lobbying | DOD, Commerce, USTR, State |

| Rio Tinto | $2.1M | Self + Lot Sixteen + CGCN + Avoq + Torres + Holland & Hart | Commerce, USTR, Interior, Treasury, Energy, State, NSC, EXIM Bank |

| Nuclear Energy Inst. | $1.9M | Self + Miller Strategies | Energy, DOD, State, Commerce |

| SEMI | $1.5M | Self-lobbying | Commerce, USTR, DOD |

Mining/Processing Firms with Targeted Lobbying

These are smaller companies whose lobbying is surgically aimed at the agencies deciding their fate:

| Commenter | Spend | Lobbying Firms | Notable Target |

|---|---|---|---|

| Cameco (uranium) | $1.5M | Self + Bracewell + Dentons | Energy, DOD, State, NRC, NSC |

| Centrus Energy (enrichment) | $1.4M | Self + Kountoupes Denham + Bridge + Compass + CT Group + Bluewater | Commerce, Energy, White House |

| Johnson Matthey (PGMs) | $1.0M | Self + Mindset Advocacy + Monument Advocacy | Commerce, USTR, Interior, NSC, White House |

| Niron Magnetics (iron nitride magnets) | $560K | Self + Holland & Knight | DOD, Energy, Commerce |

| MP Materials (rare earths) | $500K | Self + American Defense Int'l + Strategic Marketing + J.A. Green | DOD, Commerce, State, GSA |

| Sila Nanotech (silicon anodes) | $290K | Holland & Knight + Venn Strategies + K&L Gates | Commerce, USTR, DOD, Energy |

| Nyrstar (zinc) | $252K | Cassidy & Associates + North Star + Guidepost | Commerce, USTR, Energy, Interior, BLM |

| Energy Fuels (REEs/uranium) | $240K | Bose Public Affairs Group | Commerce, USTR, Energy, Interior, DOD |

| IperionX (titanium) | $220K | Self-lobbying | Commerce, USTR, BIS directly, DOD, Energy, ITA |

| Trafigura (nickel trader) | $160K | Ragnar Group | DOD, Energy, State |

| Commenter | Spend | Lobbying Firms | Notable Target |

|---|---|---|---|

| Cameco (uranium) | $1.5M | Self + Bracewell + Dentons | Energy, DOD, State, NRC, NSC |

| Centrus Energy (enrichment) | $1.4M | Self + Kountoupes Denham + Bridge + Compass + CT Group + Bluewater | Commerce, Energy, White House |

| Johnson Matthey (PGMs) | $1.0M | Self + Mindset Advocacy + Monument Advocacy | Commerce, USTR, Interior, NSC, White House |

| Niron Magnetics (iron nitride magnets) | $560K | Self + Holland & Knight | DOD, Energy, Commerce |

| MP Materials (rare earths) | $500K | Self + American Defense Int'l + Strategic Marketing + J.A. Green | DOD, Commerce, State, GSA |

| Sila Nanotech (silicon anodes) | $290K | Holland & Knight + Venn Strategies + K&L Gates | Commerce, USTR, DOD, Energy |

| Nyrstar (zinc) | $252K | Cassidy & Associates + North Star + Guidepost | Commerce, USTR, Energy, Interior, BLM |

| Energy Fuels (REEs/uranium) | $240K | Bose Public Affairs Group | Commerce, USTR, Energy, Interior, DOD |

| IperionX (titanium) | $220K | Self-lobbying | Commerce, USTR, BIS directly, DOD, Energy, ITA |

| Trafigura (nickel trader) | $160K | Ragnar Group | DOD, Energy, State |

The Key Finding: IperionX Lobbies BIS Directly

Of all the commenters, IperionX Critical Minerals LLC is the only one that PoliStack's graph shows lobbying the Bureau of Industry and Security (BIS) directly — the exact agency running this Section 232 investigation. They also lobby the International Trade Administration (ITA), which administers tariff determinations. Their public comment called for tariffs on titanium products and government support for new domestic titanium processing technology.

Lobbying Firm Clusters

Several lobbying firms represent multiple commenters on this docket, creating influence hubs:

- Holland & Knight → Sila Nanotechnologies, Niron Magnetics (both want tariff protection for domestic alternatives)

- Cassidy & Associates → Nyrstar, American Clean Power (different sides — Nyrstar wants zinc tariffs, ACP wants phased battery tariffs)

- Lot Sixteen → Rio Tinto, American Clean Power (Rio Tinto wants targeted measures, ACP wants delays)

- Strategic Marketing Innovations → MP Materials, Nucor (both favor domestic production incentives)

The Influence Math

The 28 organizations that both commented on BIS-2025-0025 and have active 2025 lobbying operations are spending a combined $56M+ on lobbying in 2025 — and that's just the commenters captured in PoliStack's graph. Add the broader lobbying ecosystem (U.S. Chamber at $70M, Business Roundtable at $33.5M, American Chemistry Council at $18.9M, Boeing at $11.3M) that's lobbying on Section 232 issues without filing on this specific docket, and the total influence spend touching this EO is well over $150M.

The dominant government targets are Commerce/BIS (the investigating agency), USTR (trade remedies), DOD (defense procurement and DPA funding), and Energy (nuclear fuel and DPA Title III). Every commenter with lobbying activity is covering at least 3 of these 4 agencies.

Data sources: PoliStack Neo4j graph (ExecutiveOrder, Regulation, PublicComment, Bill nodes), Congress.gov API, Federal Register/regulations.gov, Senate LDA lobbying disclosures